For more than four decades both Prof. Aswath Damodaran and Prof. Bradford Cornell have stressed the importance of the equity risk premium (ERP) for evaluating the stock market. This video dives into the calculations to explain why understanding the role of the ERP is critical for investors.

Economic Insights

CORNELL CAPITAL GROUP

Stock Price Performance in Review We begin our Q3 2024 memo with a look back over the last ten years. The chart below plots both the standard S&P 500 index, which is value-weighted, and the equal weighted S&P 500 index over the last decade. The major difference between the two indexes is that large companies in

The combination of P/E multiples and earnings determines stock prices – its basic math. In our last episode of Reflections on Investing we looked at earnings, now we add in the role of the multiple. Hello! Welcome back to Reflections on Investing with the Cornell Capital Group. This week, we’re going to follow up on

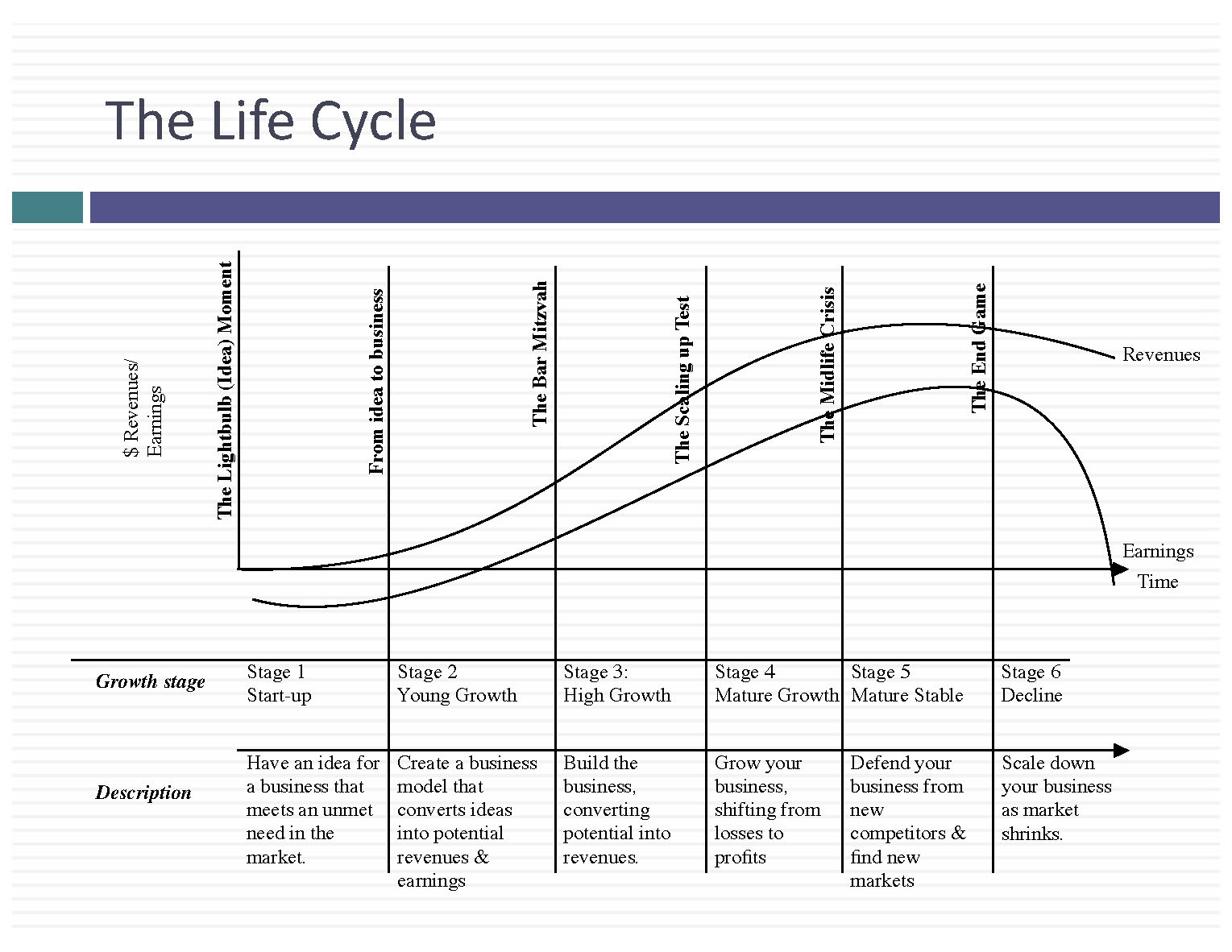

Download PDF Aswath Damodaran writes about what he calls the corporate life cycle.[1] He illustrates the life cycle with the graphic as shown below. From a valuation perspective, Damodaran’s corporate life cycle can be broken down as follows. In the first part, Stage 1 and Stage 2, the company has no meaningful earnings and limited

The performance of the market was remarkable in the second quarter. Driven by the Magnificent 7 tech stocks, for which the total return was 16.5%, the total return for the S&P 500 was 4.3%. What was remarkable was not the gain per se, the returns were healthy but by no means unprecedented, but the valuation

A common refrain is that to get more return you have to bear more risk. But what exactly is risk? We revisit this important issue. As part of the work leading to his Noble Prize, William Sharpe noted that in equilibrium all investors should hold some combination of the risk-free asset and the market portfolio.

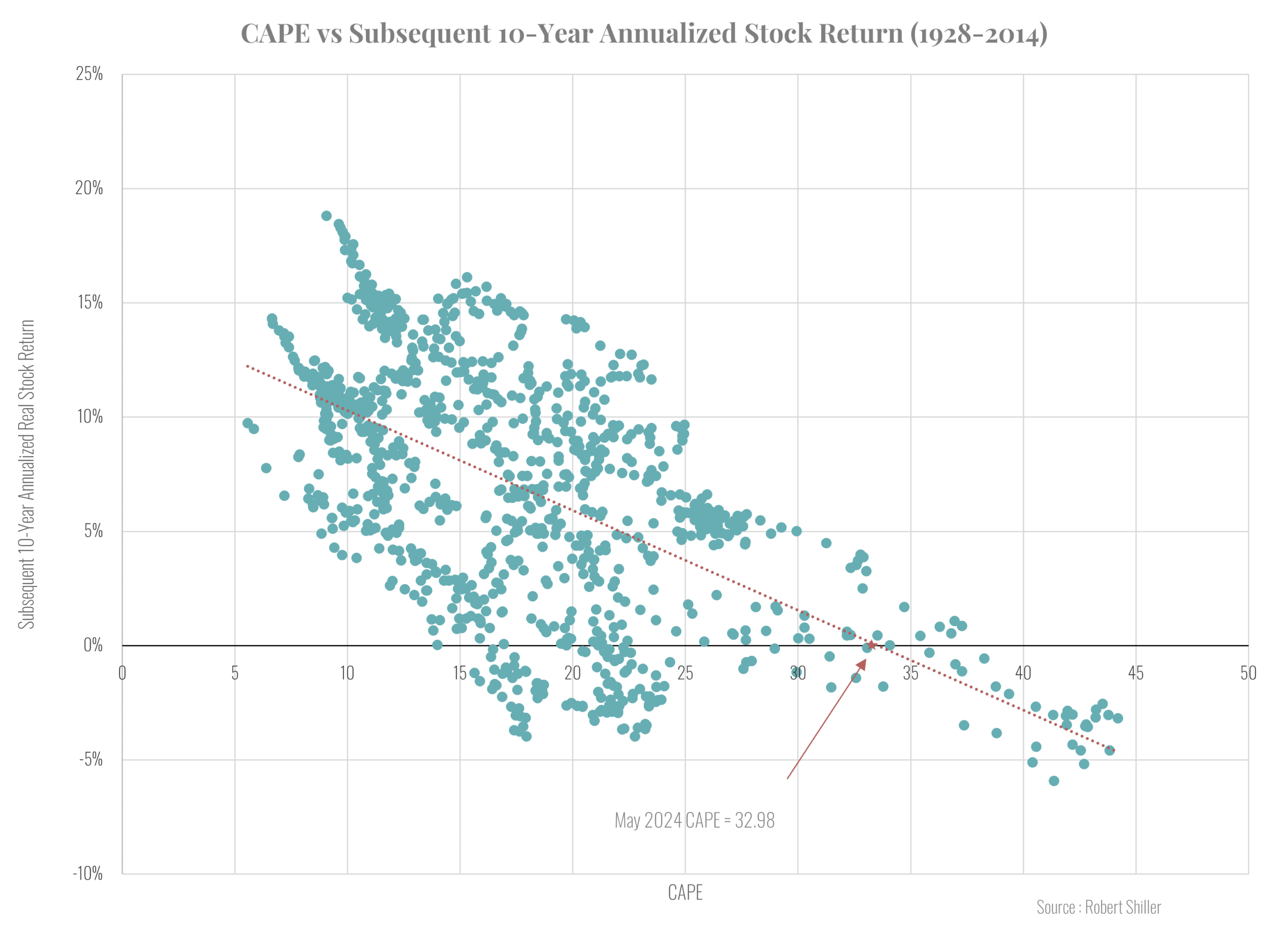

Download PDF With stock prices at near record highs relative to measures like earnings or cash flow, many leading analysts have predicted meager returns over the next decade. Some have even suggested the return on the S&P 500 could be negative over the upcoming decade. Others have raised the possibility of a short-term collapse of

The S&P 500 ended the year 2023 at 4,769. During December, several leading financial firms were asked for their forecasts for the year-end 2024. The results are shown below. The most optimistic forecasts were by Fundstrat (a well-known bullish firm), Oppenheimer, and Yardeni. Considering the strong returns during 2023, four major firms, including Morgan Stanley

Professor and Nobel Prize winner Eugene Fama put forth the efficient market hypothesis and based on that concept Warren Buffet suggested that holding a passive investment in the S&P 500 was the best advice for most investors. If the market were efficient and if passive investing was best for everyone, how can that be reconciled

Page [tcb_pagination_current_page] of [tcb_pagination_total_pages]