The Economics of Good Enough: Competition, Tokenomics, and the AI Value Chain

Competition is making artificial intelligence cheaper and better for everyone who uses it — and systematically dismantling the pricing power its investors are counting on. A look at what that means for barriers to entry, tokenomics, and the rest of the AI value chain.

In an earlier note, we argued that the largest technology companies are trapped in a prisoner’s dilemma: each must invest enormous sums in AI infrastructure because the cost of abstaining and being wrong is existential, while the cost of investing and being wrong is merely measurable. When every player makes the same bet at the same scale, the competitive advantages cancel out, and what remains is mutual margin compression.

That analysis concerned the spending decision. This note concerns what happens next — what competition does to the economics of artificial intelligence once the infrastructure exists. Eighteen months of evidence are now in, and they point in one direction: the same competitive forces that make the technology cheaper and better for its users are systematically dismantling the pricing power its investors are counting on. The mechanism runs through every layer of the AI value chain, and it is worth tracing carefully.

”The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage.” — Warren Buffett, 1999

The Big Market Delusion, Once More

Long-time readers will recognize the framework. The hallmark of a big market delusion is that all the firms in an evolving industry rise together even though they are often direct competitors. Each is priced as if it will be a major winner in the new big market — a fallacy of composition, because the sum of the parts cannot be greater than the whole. We watched this play out in social media, then in electric vehicles. We have argued since 2023 that AI may be the third act, and the principle that governs all such episodes is unchanged:

A new technology does not translate into value creation for the companies building it unless it produces returns on invested capital in excess of the cost of capital. To earn excess returns, there must be barriers to entry that prevent competitors from adopting the technology, entering the business, and driving the return on invested capital back down to the cost of capital.

Three years later, the question “what are the barriers to entry?” is no longer theoretical. The industry has now spent enough money, and operated long enough at commercial scale, that we can begin to answer it with evidence rather than conjecture.

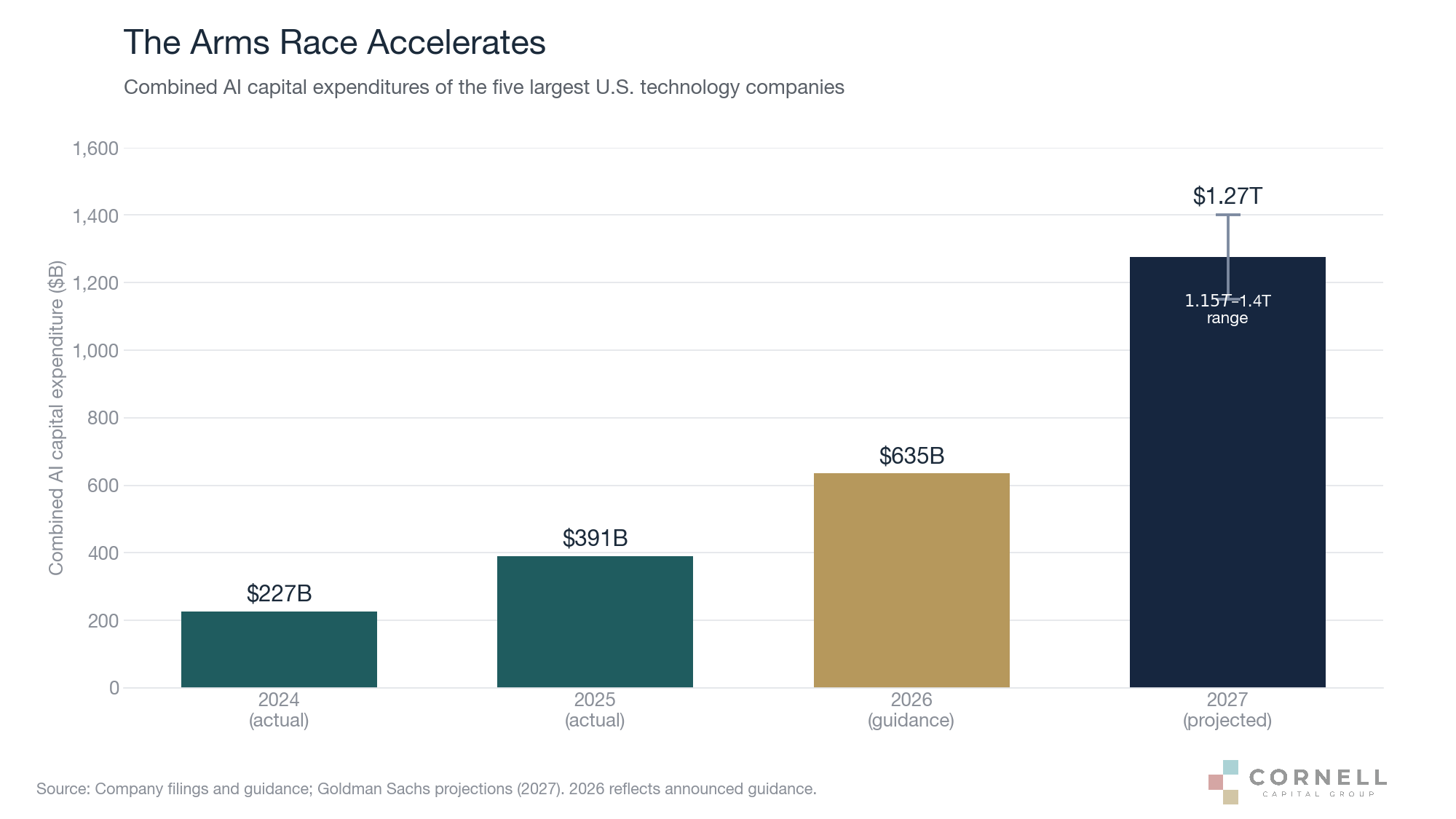

First, the scale of the commitment. The five largest U.S. technology companies increased their combined AI capital expenditures from roughly $227 billion in 2024 to $391 billion in 2025, with 2026 guidance above $600 billion. Goldman Sachs projects the total will reach $1.15 to $1.4 trillion by 2027, and roughly $7.6 trillion cumulatively by 2031.

Spending of this magnitude is rational only if it purchases something durable. The thesis underlying it — sometimes stated explicitly, more often simply assumed — is that scale itself is the moat: the largest clusters train the best models, the best models win the customers, and the flywheel compounds. It is precisely this thesis that the past eighteen months have called into question.

The Barrier That Wasn’t

The first crack appeared in January 2025, when the Chinese lab DeepSeek demonstrated capabilities competitive with frontier U.S. models at a fraction of the training cost. Nvidia lost $589 billion of market value in a single session — the largest one-day loss in U.S. market history. The stock recovered; the question it raised did not.

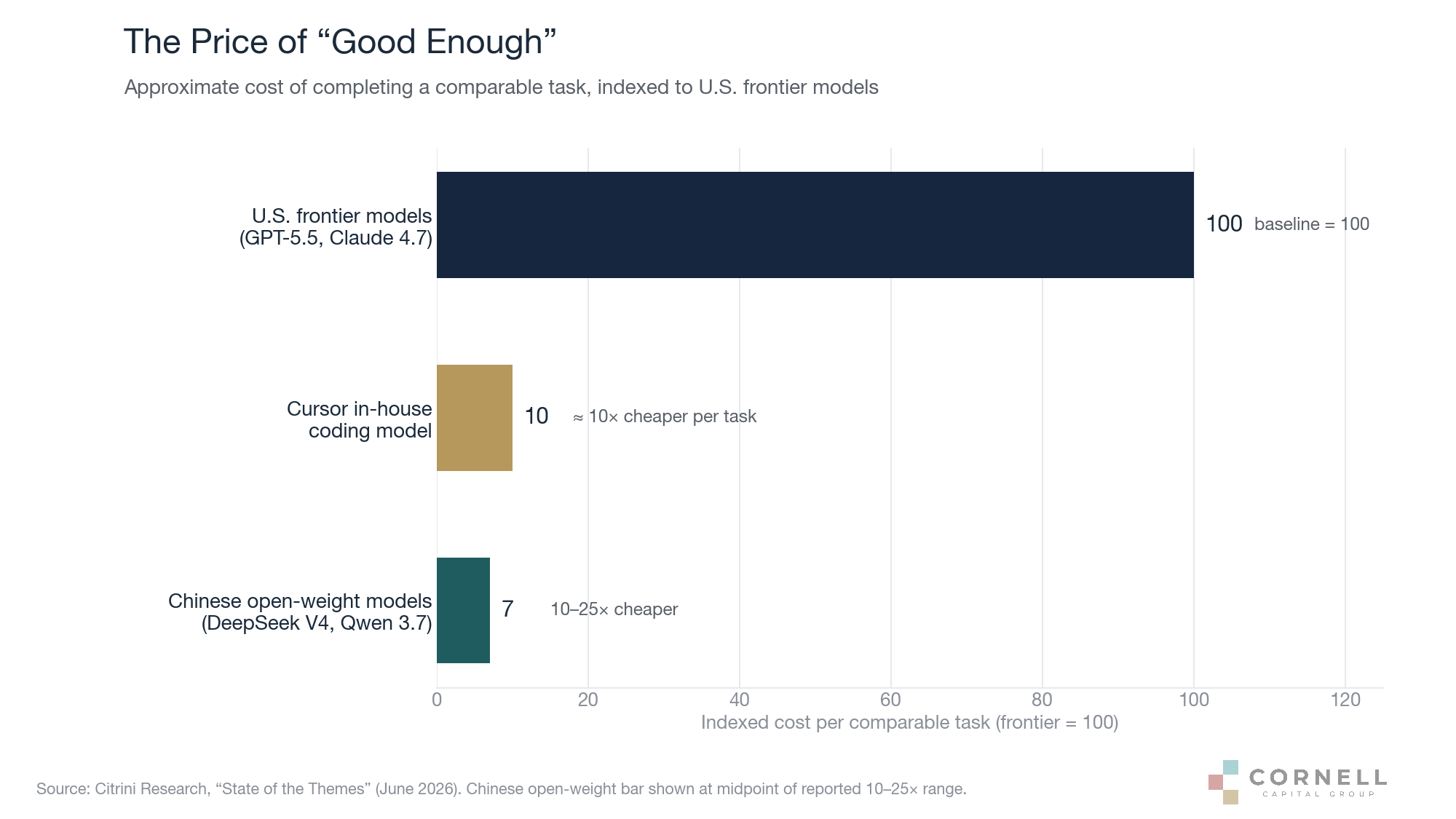

That question has since been answered more thoroughly than the optimists hoped. By mid-2026, Chinese open-weight models — DeepSeek V4 and Qwen 3.7 — deliver performance adequate for the majority of commercial workloads at prices 10 to 25 times below the U.S. frontier labs. After the V4 launch, DeepSeek surpassed Anthropic in token volume on OpenRouter, a marketplace where developers route each request to whichever model offers the best price for the job. Nor is the pressure only foreign: Cursor, an application company, built an in-house coding model that completes comparable tasks at roughly one-tenth the cost of the frontier models it previously rented.

The pattern is familiar from every prior technology cycle: the frontier advances, but the frontier premium is perishable. What a frontier model alone can do today, a model costing a tenth as much will do within a year. A barrier to entry that must be rebuilt every twelve months at escalating cost is not a barrier. It is a treadmill.

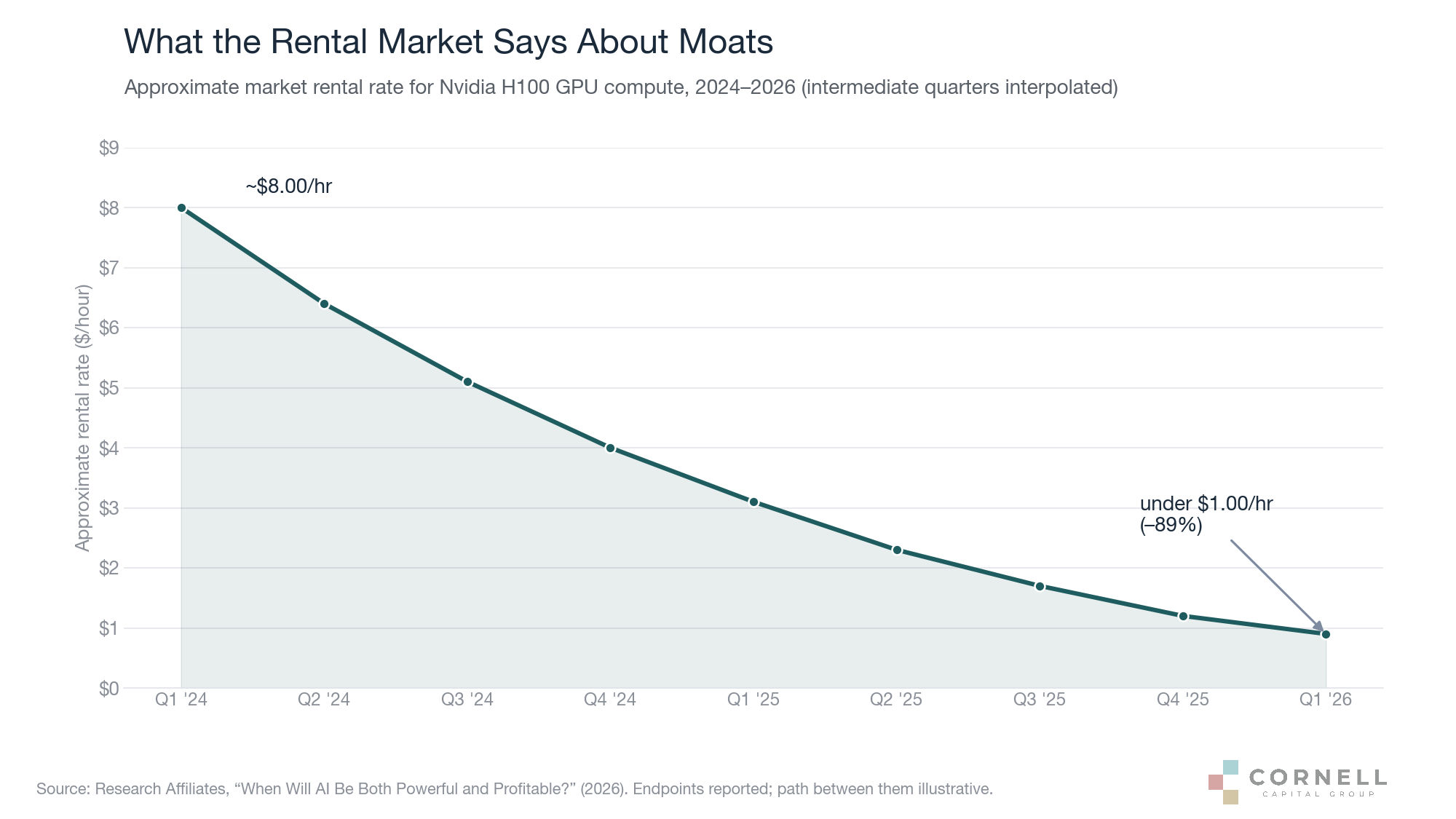

The hardware market is delivering the same verdict. The market rental rate for Nvidia’s H100 — the chip that anchored the 2023–24 build-out — has fallen from roughly $8 per hour in 2024 to under $1 in early 2026. Owning last year’s compute confers no pricing power at all.

This price collapse carries a second, less appreciated implication. Hyperscalers depreciate AI hardware over five to six years, but Nvidia now ships on an annual product cycle with step-function performance gains, which argues for an economic life closer to three. Under a three-year assumption, only about one-third of projected 2026 hyperscaler capex represents genuine capital formation; the rest merely replaces equipment that has become economically obsolete. Goldman Sachs identifies the assumed useful life of AI silicon as the single most influential variable in the entire build-out — and notes that even the data centers themselves, codesigned around particular chip generations at $15–20 million per megawatt, may be obsolete for next-generation hardware within a few years. This is not capital deepening. It is capital churn, and reported earnings that rest on six-year depreciation schedules are overstating the difference.

Tokenomics: When the Customer Saw the Bill

If competition is eroding barriers on the supply side, the demand side has just lived through something more abrupt: the end of subsidized intelligence.

Through 2025, flat-rate subscriptions concealed the true cost of AI from the people using it. The concealment was expensive for the sellers — by some estimates, the leading labs were at one point delivering $8 to $13.50 worth of tokens for every $1 of subscription revenue. That arrangement could not survive contact with the capital markets, and in the first half of 2026 it ended almost simultaneously across the industry: OpenAI moved to usage-based pricing on April 2, Google on May 19, and Microsoft on June 1, while Anthropic introduced a new tokenizer that consumes roughly 35% more tokens for identical text.

The enterprise response was immediate, and it is the most instructive dataset the AI economy has yet produced. Uber burned through its annual token budget in four months and capped spending at $1,500 per employee per month. T-Mobile capped at $2,000. Brex limited engineers to $500 per week and everyone else to $5. One company reportedly received a single month’s overage bill of $500 million. A KPMG survey found that 22% of enterprises had no visibility into their AI costs until the bill arrived. The shift has a name that will likely stick: the industry has moved from “tokenmaxxing” to “tokenpanic.”

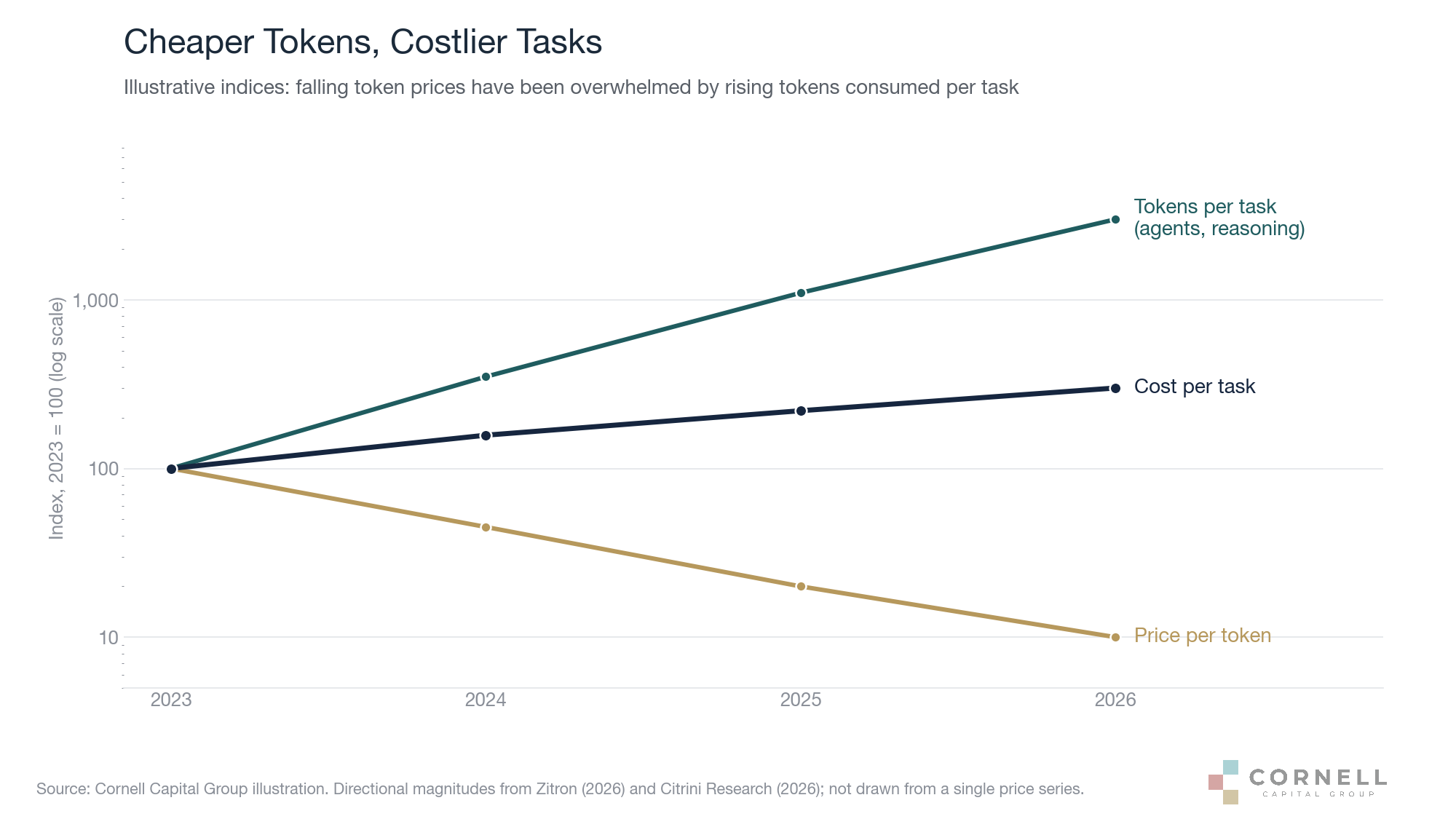

Two structural facts emerged from the panic. The first is the paradox at the heart of AI’s unit economics: the price per token keeps falling, but agentic workflows and reasoning models have multiplied the tokens consumed per task far faster. The cost of a task — the thing a business actually buys — has been rising even as the cost of a token falls.

The second fact is what visible costs do to buyer behavior. When AI was effectively free, nobody asked whether the frontier model was necessary. Now that every prompt has a price, procurement discipline has arrived, and with it the question that destroys premium pricing in every maturing market: is the cheaper one good enough? For the majority of workloads — summarization, classification, routine code, internal search — the answer is increasingly yes. Frontier models will retain their premium only for specialized work, while “good enough” captures the standard use cases. This is not a temporary feature of the adoption curve. It is what competition is. The 10-to-25-times price gap is the mechanism by which the return on invested capital of the frontier labs is being driven toward — and currently sits well below — their cost of capital.

The return-on-investment evidence on the customer side completes the picture. A Bain survey of 951 executives at companies with over $100 million in revenue found that only 4% achieved cost reductions exceeding 30% from AI deployments, while 44% are funding their next wave of AI investment from savings that have not yet materialized. Bain’s own summary is admirably blunt: “The technology worked. The value didn’t arrive.”

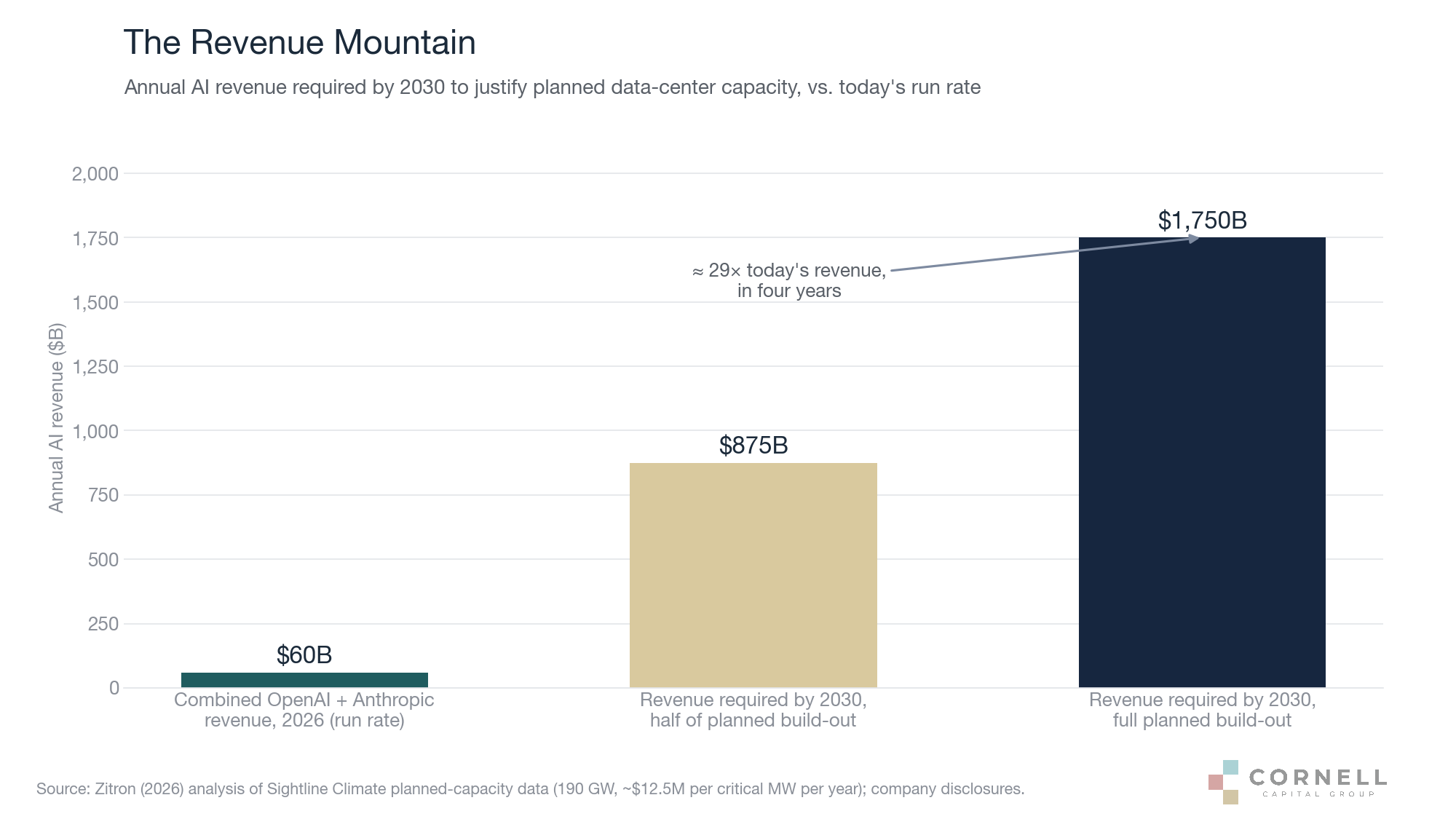

The Arithmetic of the Build-Out

Set against this demand picture, the supply commitments are extraordinary. Planned AI data-center capacity stood at roughly 190 gigawatts as of February 2026, at a construction cost Nvidia itself estimates at $80–100 billion per gigawatt. Even at conventional utilization assumptions, capacity on that scale requires on the order of $1.75 trillion in annual AI revenue by 2030 to earn its keep — against a combined OpenAI and Anthropic run rate of roughly $60 billion today. Even if only half the announced capacity is built, the revenue requirement is nearly fifteen times the current run rate of the two firms that constitute most of the market.

And “most of the market” is barely an exaggeration. OpenAI and Anthropic account for an estimated 89% of AI startup revenue and 70–90% of hyperscaler AI compute demand; Nvidia derives 54% of its revenue from three customers. The demand justifying the build-out is, to a remarkable degree, circular: hyperscalers invest in the frontier labs, the labs spend the proceeds on hyperscaler compute, and the hyperscalers buy Nvidia hardware to supply it — each leg of the triangle citing the others as evidence of demand. Meanwhile OpenAI’s first-quarter 2026 operating margin was negative 122% on a non-GAAP basis, and both leading labs face funding requirements in the hundreds of billions of dollars over the next twelve to eighteen months to honor compute commitments already signed.

We need not adopt the most bearish reading of these figures to make the narrower point: the revenue mountain must be climbed by firms whose pricing power is being competed away while they climb it. The build-out math assumes monetization at premium prices; the competitive dynamics described above assume away the premium. Both cannot be true.

Downstream: Who Bears It, Who Escapes It

The consequences are not evenly distributed along the AI chain.

Nvidia has been the great beneficiary of the arms race, and its annual product cadence is a genuinely formidable competitive position. But that same cadence is what shortens the economic life of its customers’ assets, and 54% revenue concentration in three customers means Nvidia’s income statement is, in effect, a derivative of its customers’ willingness to keep absorbing accelerated obsolescence. Should capex growth merely flatten, the multiple paid for cyclical-peak earnings will be re-examined. Dominance of a market whose economics are deteriorating is a smaller prize than the price implies.

The hyperscalers face the prisoner’s dilemma in its purest form. They cannot stop spending — the game theory forbids it — but the spending increasingly resembles a defensive toll rather than an investment. The tell is in capital allocation: mega-cap share buybacks collapsed 74% year-over-year in the fourth quarter of 2025 as cash was redirected to capex. Owner earnings are being diverted into assets with three-to-five-year economic lives depreciated over five to six years, in pursuit of revenue that the competitive dynamics above suggest will carry thinner margins than the businesses funding it. Investors should watch depreciation schedules and disclosed useful-life assumptions as closely as they watch revenue guidance; that is where this story will surface in the financial statements first.

The frontier labs occupy the most precarious position: negative unit economics, a price umbrella under attack from the open-weight models beneath them, and compute obligations — $770 billion in OpenAI’s case, $375 billion in Anthropic’s — that assume growth rates of several hundred percent sustained for years. They are simultaneously the customers justifying the hyperscalers’ capex and the suppliers whose pricing power is eroding fastest.

The financing chain deserves more attention than it receives. Oracle’s Stargate commitments alone involve 7.1 gigawatts of capacity costing an estimated $340–700 billion, supported in part by founder share-collateralized borrowing. When the marginal data center is financed against the revenue projections of customers who are themselves unprofitable, credit risk has entered a system that equity investors are still analyzing as a growth story. This rhymes with the late-1990s telecom build-out, where the vendors and carriers financed each other until neither could.

The physical layer — power, grid equipment, cooling, fuel — is where the barriers to entry actually reside. Large power transformers carry three-to-four-year lead times; data-center power infrastructure spending is projected to grow from $16.5 billion in 2025 to $27.8 billion in 2026; some suppliers are sole-source by regulatory licensing rather than by technological lead. A bottleneck that cannot be prompted away is a better moat than a benchmark score. The caveat is symmetry: businesses whose demand floor depends entirely on the AI capex cycle inherit that cycle’s risk, so the distinction that matters is between firms with demand independent of the build-out and firms that are pure expressions of it.

The application layer and the end user are the likely winners, for the oldest reason in economics: when an input gets cheaper, the surplus flows to whoever uses the input, not whoever produces it. This was the conclusion of our prisoner’s dilemma analysis — the real winners may not be the companies laying the pipe, but the ones who figure out what to run through it — and everything since has strengthened it. Every price war among the model providers is a gift to the businesses built on top of them.

Implications for Investors

Four conclusions follow directly from the framework.

First, separate the question “will AI work?” from the question “will AI investments pay?” They are routinely conflated, and they have opposite sensitivities to competition. Intense competition makes the technology better and cheaper — and makes the returns on the capital behind it worse. History’s verdict here is consistent: automobiles, commercial aviation, railroads, and fiber-optic networks all transformed society while destroying, at one point or another, most of the capital that built them.

Second, interrogate reported earnings. Where AI hardware is depreciated over five or six years against a three-year economic life, current earnings are borrowing from future write-downs. The gap between accounting depreciation and economic obsolescence is the single largest soft spot in mega-cap income statements today.

Third, apply the pricing-power test to every AI claim. The question is not whether a company uses AI, or even whether it leads in AI. The question is whether it could raise prices without losing the workload to an alternative that is 90% as good at 10% of the cost. Very few participants in the chain can currently answer yes. Those that can — sole-source physical suppliers, businesses with genuine switching costs at the application layer, owners of scarce distribution — are where durable value is most likely to accrue.

Fourth, patience remains warranted. Until clearer evidence emerges of sustainable barriers to entry and returns on invested capital meaningfully above the cost of capital, we are content to remain on the sidelines rather than speculate on how this revolution will ultimately be monetized. The evidence that has emerged since we first made that argument — tokenpanic, the good-enough price gap, the collapse in GPU rental rates — points the other way: toward an industry whose competitive structure is hardening against excess returns at precisely the moment its capital commitments are largest.

Conclusion

None of this is an argument that artificial intelligence will fail. It is an argument that the technology’s success and its investors’ returns are separate questions joined by a single variable: barriers to entry. Competition is the mechanism by which AI’s benefits will reach the broader economy — cheaper intelligence, embedded everywhere, eventually priced like a utility. It is also the mechanism by which the excess returns assumed in today’s valuations are competed down to the cost of capital. The big market delusion has never been a claim that the market isn’t big. It is the observation that everyone cannot win it simultaneously — and that the bigger the market looks, the more capital arrives to ensure no one wins it outright.

The cheaper intelligence becomes, the better for the world — and the steeper the mountain for those who paid for it to be expensive.

A note on sources: the figures and estimates in this piece are drawn from third-party research — including Goldman Sachs (“Tracking Trillions”), Research Affiliates (“When Will AI Be Both Powerful and Profitable?”), Citrini Research (“State of the Themes,” June 2026), and commentary by Ed Zitron — and have not been independently verified by Cornell Capital Group. Company-level capex, revenue, and pricing figures reflect the most recent disclosures and guidance available as of publication and are subject to revision.